Editor’s Note: This is the second series in our exploration of why traditional law is collapsing and what’s replacing it. If you’re new here, start with The Last Hour for the big picture of why legal infrastructure is overtaking law firms, then read Why Legal Thinking Is Backwards to see the mismatch between what businesses hire lawyers to do and what firms actually deliver.

Across every industry, incumbents trapped in legacy revenue models have failed to survive disruptive innovation. Law is no exception.

The question isn’t whether BigLaw sees the threat. It does. The question is whether it can adapt without dismantling the very economics that keep it alive. The answer is clear: it cannot.

The Disruption Playbook: What History Teaches

Harvard Business School professor Clayton Christensen's theory of disruptive innovation provides the most accurate framework for understanding BigLaw's inevitable collapse. In "The Innovator's Dilemma," Christensen identified why even the most successful, well-managed companies consistently fail when facing certain types of technological change.

The pattern is predictable, and BigLaw exhibits every characteristic of vulnerable incumbents.

The Disruption Framework

Christensen distinguished between two types of innovation:

Sustaining Innovation improves existing products along performance dimensions that mainstream customers value. Incumbents usually win these battles because they have resources, relationships, and expertise.

Disruptive Innovation initially offers worse performance on traditional metrics but typically provides simplicity, convenience, or affordability. It starts at the margins, serving the customers incumbents ignore or dismiss as unprofitable.

The crucial insight is that incumbents can't respond to disruptive innovation without destroying their business models. They're trapped by the very capabilities that made them successful.

While incumbents focus on sustaining innovation (improving core offerings for premium customers) disruptors optimize for new performance dimensions.

The incumbents scoff. They focus on high-margin customers who demand sophisticated solutions. As disruptors capture low-end markets, incumbent profitability improves because their average margins increase. For the incumbent, this looks like strategic success while it's actually selective collapse.

But disruptors don't stop at the low end. They improve their offerings systematically. By the time incumbents recognize the threat, disruptors have established market positions and cost structures that make incumbent response impossible.

Incumbents see the threat but cannot respond because their cost structures, margin expectations, and reward systems aren't just aligned with the status quo, they're hard coded to protect it. To chase the disruptive model would mean dismantling the profitable systems that still generate current revenues.

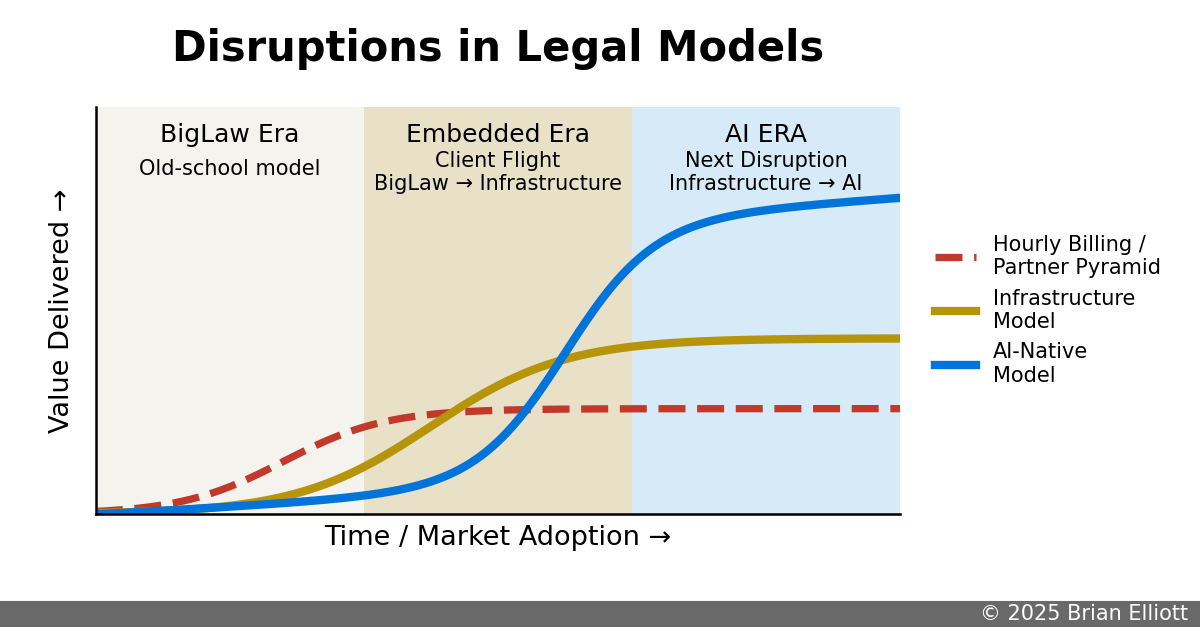

In law, the incumbents are obvious: BigLaw’s partner pyramids and hourly billing. The disruptors, embedded counsel models and alternative legal service providers (ALSPs), are already here, delivering speed, judgment, and alignment that clients can’t get from the pyramid. The next wave is even more radical: clients embedding legal AI and AI-native law firms that will open market BigLaw has never served. Hold that frame as we look at other industries that played this story before.

Kodak: Sustaining Innovation Trap

Kodak exemplifies incumbent failure despite technical superiority and resource advantages. When Kodak engineer Steven Sasson invented the digital camera in 1975, company executives immediately understood its revolutionary potential. They had the patents, the technical expertise, and the financial resources to dominate digital photography.

But digital photography was classic disruptive innovation. Early digital cameras offered terrible image quality compared to film, they were expensive and complex to use, and they provided no immediate prints. They seemed inferior on every dimension that serious photographers cared about.

However, digital offered different benefits: immediate image review, unlimited shots without film costs, and easy electronic sharing. These advantages initially appealed only to technical enthusiasts and cost-conscious casual users. Kodak considered these markets to be beneath their high-quality film business.

Kodak's business model made disruption response impossible. Film and photo processing generated 60% of profits while representing only 25% of revenues. Digital cameras would be one-time hardware sales with no recurring revenue. Even winning the digital camera market would destroy Kodak's profitability. So Kodak pursued sustaining innovation: better film quality, faster processing, more convenient packaging.

Meanwhile, companies like Canon and Sony, unburdened by film economics, optimized digital cameras for performance rather than profit protection. They improved image quality, reduced costs, and expanded market reach. By the time digital quality matched film performance, these competitors controlled market share that made Kodak's technical advantages irrelevant.

Kodak filed for bankruptcy in 2012. The company that invented digital photography was destroyed by digital photography because sustaining innovation thinking prevented disruptive innovation response.

Kodak's collapse mirrors BigLaw's current predicament: they possess superior technical knowledge (legal expertise), control premium market segments (Fortune 500 clients), and face disruptive technology (AI and ALSPs) that threatens their core revenue model (billable hours). Like Kodak, BigLaw firms recognize the threat but cannot respond without destroying the economics that fund their current success.

But this pattern is not unique to technology companies, the systematic destruction of the American integrated steel industry reveals something more disturbing: entire industries can follow this trajectory simultaneously, with incumbents actually celebrating the market losses that signal their doom.

Steel: The Mini-Mill Disruption

The American steel industry provides an even clearer example of Christensen's framework in action. Integrated steel companies like U.S. Steel and Bethlehem Steel possessed every conceivable advantage: decades of steelmaking expertise, established customer relationships, extensive distribution networks, and vast financial resources.

Mini-mills represented classic low-end disruption. Electric arc furnace technology could only produce low-grade steel suitable for wire rod and rebar products that integrated companies considered loss-leader commodity markets beneath their sophisticated capabilities.

The incumbents were delighted to cede these low-margin segments. Rebar generated minimal profits compared to high-grade automotive and aerospace steel. By abandoning commodity markets and focus on premium products integrated steel companies actually improved profitability and thrilled shareholders.

But mini-mills like Nucor weren't trying to compete with integrated steel, they were building a different business model. Electric arc furnaces required minimal capital investment, could operate profitably at small scale, and enabled rapid response to market changes. They used low-margin markets to perfect technology, reduce costs, and build operational expertise.

Once established, mini-mills moved upmarket systematically. One by one, over a period of years, they captured construction steel, then structural steel, then sheet steel for appliances and automotive applications. Each market expansion eliminated the high-margin business that the massive integrated mills needed to support their fixed costs.

The incumbents couldn't respond because their business model, dependent on large capital investments in integrated facilities, required the high-margin markets that mini-mills were systematically making unprofitable. Adapting to mini-mill economics would require abandoning billions in infrastructure and thousands of jobs.

The steel industry's destruction reveals BigLaw's future with chilling precision. Like integrated steel companies, BigLaw dismisses 'low-value' and ‘loss-leader’ legal work (document review, basic contract analysis, routine compliance) as beneath their sophisticated capabilities. Like steel executives, BigLaw partners celebrate when competitors capture these unprofitable segments, allowing firms to focus on premium services for sophisticated clients. But AI-powered legal services are following the mini-mill playbook: perfecting technology in commodity markets before moving upmarket to capture the high-margin work that funds partnership economics. The cost/structure advantages that made mini-mills unstoppable are identical to the efficiency gains that make AI legal services inevitable.

Textbook Incumbent Vulnerability

BigLaw exhibits every vulnerability that Christensen identified.

Resource Allocation Processes That Favor Sustaining Innovation. Law firms invest in sustaining innovations that improve traditional legal delivery: better legal research tools, more sophisticated document review platforms, and enhanced project management systems. They cannot invest in disruptive technologies that eliminate billable work because their economic model depends on maximizing billable hours.

When firms do experiment with disruptive ideas, they sandbox them so they never threaten the partner pyramid. WilmerHale’s SixFifty (automated forms spun out), CooleyGo (free startup documents used as marketing), and Flex by Fenwick (an ALSP unit structurally separated from core Fenwick) all show the same pattern: innovation at the edges, carefully insulated from the billable-hour machine. They prove firms aren’t blind to disruption—they just can’t let it touch the economics that keep them alive.

Customer Dependency on High-Margin Segments. BigLaw firms optimize for Fortune 500 clients who demand sophisticated legal analysis and accept premium pricing. They dismiss “low-value” work like reviewing NDAs, cleaning up equity records, drafting employee policies, checking privacy compliance boxes, and turning vendor contracts quickly. But these are exactly the pressure points where disruptive innovation takes root because most businesses need speed, predictability, and cost control more than prestige legal analysis.

Performance Metrics That Reward Status Quo. Law firms measure success through metrics that reward traditional service delivery: utilization rates, profits per partner, and revenue growth. They cannot measure success through client problem elimination or process automation because those outcomes threaten the work that generates measured performance.

Cost Structures That Prevent Downmarket Competition. Partnership economics require high-margin work to support partner compensation, associate leverage, and overhead expenses. Traditional law firms cannot compete in lower-margin markets even when they recognize the strategic importance because their cost structures make such competition economically impossible.

Technical Capabilities That Become Strategic Liabilities. BigLaw's legal expertise, relationship networks, and regulatory knowledge represent enormous advantages in traditional markets. But these capabilities require high-cost delivery models that disruptive competitors can avoid entirely by building different solutions optimized for efficiency rather than comprehensive coverage.

The AI Disruption Pattern

Legal AI follows the classic disruptive innovation trajectory that Christensen's framework predicts:

Initial Performance Inferiority. Early AI legal tools produce inferior analysis compared to experienced lawyers. They miss nuances, lack judgment, and require human oversight. Traditional law firms correctly dismiss them as inadequate for sophisticated legal work.

Different Performance Dimensions. But AI offers radically different benefits: instant availability, consistent quality, predictable costs, and exponential scalability. These advantages initially appeal only to price-sensitive clients and routine work that law firms consider “beneath” their capabilities.

Systematic Improvement. AI capabilities improve exponentially while traditional legal skills improve incrementally. Contract analysis that was experimental two years ago now matches junior associate performance. Legal research that required hours, even if not perfect, now happens in minutes. The performance gap is closing rapidly.

Upmarket Migration. AI tools are moving systematically from document review to contract analysis to legal research to strategic planning. Each capability expansion threatens higher-value work that law firms depend on for profitability.

Incumbent Response Paralysis. Law firms recognize the AI threat but cannot respond without destroying their business models. Every AI capability that eliminates billable work threatens the economic foundation of partnership compensation. They're trapped by the economics that enabled their current success.

The Mathematical Inevitability

Christensen's research proves that incumbent failure in disruptive innovation scenarios isn't accidental, it's inevitable when business model constraints prevent adaptation to technological change.

The failure pattern is predictable:

- Incumbents focus on sustaining innovation for high-value customers

- Disruptors optimize for different performance dimensions in “low-value” segments

- Disruptors improve systematically and move up market while incumbents protect existing economics

- By the time incumbents recognize existential threat, disruptors control markets that make incumbent response impossible

BigLaw is following this pattern exactly. They're investing in sustaining innovations that improve traditional legal delivery while dismissing AI as inadequate for "real" legal work. They're protecting partnership economics while competitors build business models optimized for client efficiency rather than lawyer compensation.

The outcome is inevitable. The structural constraints match every historical case of incumbent destruction: preservation of current economics conflicts with adaptation to technological change.

This isn’t moral failure, it’s the same mathematical inevitability Christensen documented in photography, steel, computing, telecom, and every other industry that experienced disruptive innovation. The only variable is timing. And based on the acceleration of AI capabilities, the timeline will be compressed (months or quarters, not decades) compared to historical precedents.